Beyond the GPU: The Infrastructure Plays Poised to Redefine the AI Economy

The first wave of the artificial intelligence revolution was defined by a singular, frantic pursuit: the ability to train massive large language models (LLMs). This era was characterized by a gold rush for general-purpose GPUs, creating a massive concentration of wealth in a handful of semiconductor giants. However, as the industry moves from the experimental training phase into the era of massive-scale deployment and ubiquitous inference, the investment thesis is undergoing a fundamental shift.

The bottleneck is no longer just "compute power"—it is efficiency, heat, and energy.

Wall Street analysts are increasingly looking past the headline-grabbing chipmakers to the "infrastructure layer"—the companies providing the specialized components that allow AI clusters to function at scale. Current market data suggests that while the primary chipmakers trade at historically high multiples, a subset of infrastructure players is currently undervalued, despite experiencing triple-digit year-over-year revenue growth.

The Rise of the Bespoke Silicon Architect

For the past several years, the industry has relied on versatile, general-purpose architectures. While effective, these chips are increasingly seen as inefficient for the specialized tasks required by edge-deployed AI and high-volume inference. This inefficiency creates a massive cost burden for enterprises attempting to scale.

We are seeing a decisive move toward Application-Specific Integrated Circuits (ASICs). Unlike general-purpose processors, ASICs are hardwired for specific mathematical operations, such as the matrix multiplications that underpin neural networks. This specialization allows for a significant reduction in "watt-per-inference" metrics.

Analysts point to the emerging leaders in custom silicon design as prime candidates for significant growth. These companies are not trying to replace the dominant GPU players; rather, they are providing the specialized "sidecar" chips that handle specific workloads more efficiently. As hyperscalers move toward vertically integrated hardware stacks, the demand for these design partners is skyrocketing. Because many of these firms are still in the growth phase and haven't yet reached the massive market caps of their peers, their valuations remain surprisingly accessible relative to their projected revenue trajectories.

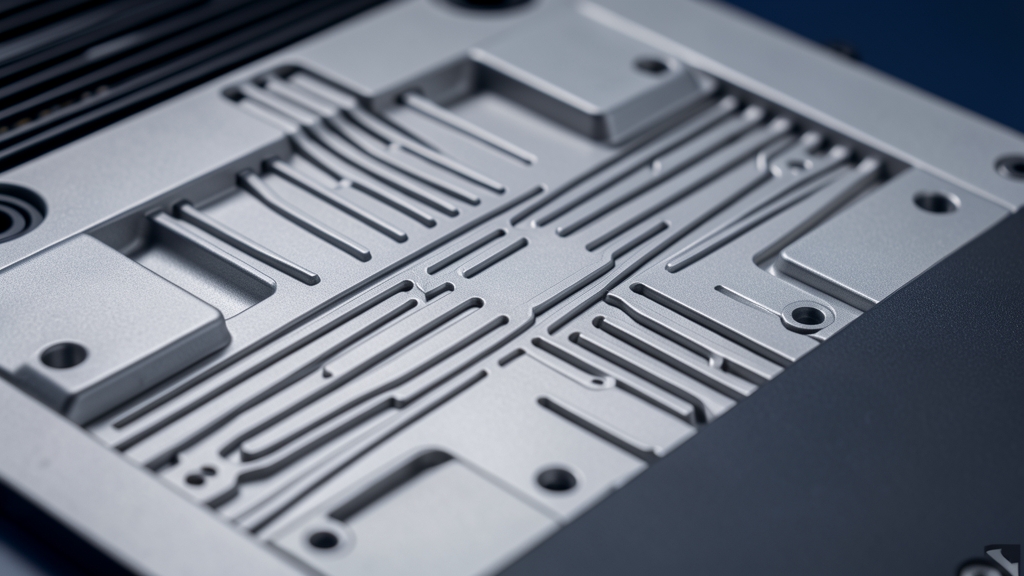

The Thermodynamic Wall: The Liquid Cooling Mandate

The second pillar of the AI infrastructure boom is perhaps the most overlooked: thermal management. The physical reality of modern data centers is hitting a thermodynamic wall. As chip density increases and power draw per rack climbs from 20 kilowatts to over 100 kilowatts, traditional air cooling—the standard for decades—is becoming physically incapable of maintaining operational stability.

When hardware runs too hot, it suffers from "thermal throttling," a state where performance is intentionally degraded to prevent physical damage. In a world where milliseconds of latency determine the viability of an AI application, thermal throttling is an unacceptable cost.

This has triggered a massive transition toward direct-to-chip liquid cooling and immersion cooling technologies. The market for these specialized thermal management systems is currently in a state of rapid acceleration. Companies specializing in high-precision coolant distribution, manifold design, and heat exchange technology are seeing their order books stretch well into the next several years.

The investment opportunity here lies in the transition from "niche" to "standard." The companies that successfully bridge the gap between legacy air-cooled data centers and the new liquid-cooled standard are positioned to capture a massive share of the capital expenditure being poured into new AI clusters.

The Energy Moat: Solving the Power Bottleneck

If silicon is the brain and cooling is the life support, then electricity is the oxygen of the AI era. The most significant constraint on the growth of artificial intelligence is no longer the availability of chips, but the availability of power. The sheer scale of the electricity required to run next-generation data centers is straining existing national grids and forcing a rethink of how power is managed and delivered.

The "energy moat" is becoming a critical competitive advantage. We are seeing a surge in demand for companies that provide modular power solutions, high-efficiency transformers, and microgrid technologies. Data center operators are no longer just looking for "cheap" electricity; they are looking for "reliable and scalable" power.

This has created a unique opening for providers of on-site power management and energy storage systems. As hyperscalers look to decouple their growth from the instability of aging public grids, the demand for localized, high-capacity power infrastructure is decoupling from broader economic trends. These companies operate at the intersection of the tech sector and the utilities sector, providing a defensive yet high-growth profile that is rare in the current market.

The Path Forward

The transition from a "chip-centric" AI market to an "infrastructure-centric" market represents one of the most significant structural shifts in the technology sector. While the initial hype cycle focused on the capability of AI, the current phase is focused on the sustainability of AI.

The companies poised to double in value are those solving the hard physical problems: How do we make the math more efficient? How do we move the heat? How do we find the power? For the discerning tech investor, the real story of the AI revolution isn't happening on the screen; it's happening in the cooling pipes, the power lines, and the specialized silicon underneath.